What Would It Look Like If the AI Bubble Popped?

摘要

文章认为 AI 领域正处于严重的投资泡沫中,今年相关资本支出高达 7500 亿至 1 万亿美元,已成为宏观经济增长的主要引擎。作者通过类比指出,AI 泡沫更像 2000 年的互联网泡沫(基础设施过度投资),而非 2008 年的债务危机。若 AI 无法在短期内证明其盈利能力或降本增效的价值,投资者补贴将枯竭,可能引发由投资缩减驱动的经济衰退,且由于当前市场集中度更高,其传染性可能比 2000 年更严重。

荐读理由

它用 dot-com 基础设施过剩与 2008 债务危机对比,指出 AI 数据中心投资驱动 1-2% GDP 增长若补贴停止需证明 ROI,否则或引发投资-led 衰退,你能据此判断 AI 产品项目的宏观风险与时机。

原文

What Would It Look Like If the AI Bubble Popped?

We're likely in a bubble of investment in AI, and it's a risk to our economy. If the stock market declines, how bad could it get? Where are there areas of contagion?

One of the consistent themes of this newsletter is how the stock market is increasingly disconnected from underlying economic activity. In the Number Go Up Rule, I traced how we increasingly run everything to ensure that market capitalization continues to increase. From the dot com boom to the subprime housing to crypto to GameStop to sports gambling, there’s an increasing mania in how we encourage speculation instead of morally valuable activity.

The flip side of this disconnect is that governance happens in crisis. Our collective understanding of finance and politics is shaped by crashes - the dot com boom, the Great Financial Crisis of 2008 and Covid, all episodes in which a crisis in one part of the system led to seemingly uncorrelated shocks elsewhere, and then political action to reorder the economy.

Today I want to ask what the popping of the AI bubble would look like, and whether it would precipitate a broader financial crash. And if it does so, what shape will it take? The right way to start is by analogy, as there are lessons from previous crashes and the governance that came out of them that we can learn from. For reasons I’ll get into, while 2008 and Covid could be useful to look at, the best analogy is dot com era.

First, it’s important to scope out what I’m not going to talk about, which is the governance of AI as a technology. It certainly matters whether we are creating a God-like system, a useful general purpose technology, or a moderately useful toy. There are many fascinating questions around copyright, liability, monopolization, and so forth, but it’s hard to offer persuasive tech policy arguments in the midst of a bubble.

In many ways, the key important question facing us today is the financing of AI, and the fact that we have placed a economy-sized bet on the enterprises claiming to focus on this technology. Just seven stocks - all linked to AI - comprise a third of the stock market, and AI capital investment is likely to be between $750 billion and a trillion dollars this year, which is big enough that it affects macro-economic growth numbers.

The stock mania we’re seeing as a result is based on the narrative that AI will be some sort of insanely profitable transformative technology. But AI is actually costly to operate, taking up a lot of electricity and expensive computing hardware. So the speculative discourse only works as long as investors subsidize the use of the technology. When that subsidy stops, these AI firms have to actually deliver value, or customers won’t buy it.

Over the past few months, that subsidy has been eroding. In May, I wrote about what happens to AI investments as the big firms raise prices to corporate America. Now it’s time for these tools to show measurable returns, either lowering costs or raising revenue. If they don’t, well, the revenues for these companies won’t deliver on the multi-trillion dollar promises they made. That may not matter in the short-term, the financial market overvalued Tesla, crypto, GameStop, and so forth. But at some point, there will be a shock.

How significant could such a shock be? Dean Baker, who called the 2008 housing crash, has an “AI bubble monitor” where he lays out the scale of what’s happening. The value of the stock market today, close to $80 trillion, is roughly twice what it was at the peak of the tech bubble. That’s 2.5 times the size of the U.S. economy. A fall back to long-term average would cut, according to Baker, $300,000 per household of paper wealth from balance sheets. Others, like AI Now’s Sarah Myers West, are drawing similar conclusions.

Now, just because the stock market is very high doesn’t mean it’s a bubble; the labor share of income is much lower than it was in 2000, meaning what used to go to workers is instead going to capital. While that’s not good for society, it actually is a good non-bubble explanation of why stocks are in nose bleed territory. Several economists recently wrote a paper to that effect, showing that stock market values are relatively constant if you account for the fact that corporations are investing less and paying their workers less, remitting what they would have put into equipment and labor to dividends and buybacks. In terms of free cash flow, which is cash to investors, they argue, the market is valued the same as it was in previous periods.

Or at least it was - now data centers are eating up all that cash flow.

But whether or not cash flow justifies valuations, we shouldn’t overthink this dynamic. A bubble popping is not some odd event. Stock market drawdowns of 50% or more are historically common, though not understood as such today in our heavily financialized economy. For instance, the April swoon that caused Trump to reverse his tariff policy was a decline of just 25%. This decline ended up putting so much political pressure on Trump that he flipped his entire administration policy.

When a sector leading our financial markets craters, the problem escapes that sector and turns into a broad-based crash. To understand what will happen, we have to trace how balance sheets transmit financial shocks across the economy, a concept called ‘contagion.’

This Friday, for instance, SpaceX is going public, leading to immense new paper wealth for a host of employees and institutions, such as universities who invested early. Just as these institutions are going to see a windfall from the SpaceX IPO, they will then become more dependent on the value of the stock. If stocks fall, then there will be contagion back to those institutions, who will then have to restructure their balance sheets, with knock-on effects to others, and so on and so forth.

2008 vs the Dot Com Boom

What kind of contagion could we see if the AI bubble deflates? Let’s compare the current moment to the two most recent financial crises, one of which was caused by mortgage-backed securities, aka debt, and the other of which was driven by a crisis in the stock market. I’m not going to include Covid, since that was an exogenous event.

Here’s a brief recap of the Great Financial Crisis, and you’ll notice some analogies to what we’re seeing today.

Is the AI Bubble a Rerun of 2008?

When I wrote my book Goliath, I noticed that the two ingredients in every financial crisis in the 20th and 21st century, from the 1920s bubble to the REIT shocks of the 1970s to the 2008 crisis, were (a) Citibank and (b) Florida real estate. And that’s because most financial shocks occur when there’s a lot of gambling with borrowed money.

Speculating with other people’s money creates a boom on the way up, but introduces significant fragility into a system. As long as things are going well, borrowing to gamble is highly profitable. But when the system starts to wobble, things go bad in a hurry. If your bet on borrowed money goes sour, you usually can’t pay back the loan, which means the person who lent the money to you can’t meet their financial obligations, and then the person who lent to that person can’t get their money, and so on, in a giant daisy chain.

The net effect is everyone tries to sell whatever they can to cover their debts, which leads to a great liquidation of assets. There’s a liquidity crisis, which means people can’t sell financial instruments for ready cash because there are no buyers. But in addition, often those assets are of questionable value in the first place. That means there’s also a solvency crisis, which means the underlying assets are just not worth enough to cover the debts. At the time of a crisis, it’s impossible to tell how much of the problem is liquidity and how much is solvency.

After a period of turbulence, a bailout or collapse, or both, we usually wind up seeing that there’s a lot of debt, more than can be paid back from the value of existing assets. So there has to be some sort of deal where all or some stakeholders take a loss.

That was the crisis of 2008. At the time there was a lot leverage, or private debt, in the system. In 2007, American households had roughly $14.5 trillion of mortgage and consumer debt. That amount had grown rapidly, escalating at 9% a year from 1998-2007 in a borrowing frenzy. By way of contrast, a much safer form of debt - Federal bonds - amounted to just $6 trillion that year. The irony is that most Wall Street people freak out about high Federal budget deficits and debt, but those actually produce safe securities, namely treasury bonds. When Wall Street generates private debt, like mortgages and commercial credit, that’s what fosters financial crisis.

As the bubble popped, the huge set of mortgage-backed instruments, and stranded housing assets, became a serious macro-economic problem. Most institutions - banks, insurance companies, pension funds, endowments - had invested in subprime mortgages and adjacent products. A significant part of the labor force was involved in building these houses.

There was another element at work. Much of this mortgage debt, and associated derivatives, was rated too highly because of systemic fraud and market manipulation. But this stuff was hidden, and the actual crisis was a surprise. Until the fall of 2008, few knew there was so much risky debt, and where it was. There was unknown contagion where, say, a bank could no longer borrow against its mortgage-backed securities, and so it couldn’t offer loans into an unrelated market, such as municipal loans. Long-standing bond markets stopped functioning. When the government refused to backstop Lehman Brothers, fear overtook Wall Street. As institutions tried to sell what they could, no one knew what anything was really worth.

The bailouts, through both the Federal Reserve and government spending, stopped the crisis, and ended up allocating the losses to the poor and middle class. The key moment in that fight was in the Presidential transition period of 2008, when Barack Obama, advised by Larry Summers and Robert Rubin, decided that homeowners would not be allowed to write down their debts, but Wall Street would get bailed out. This choice backstopped most of the institutions reliant on mortgage-backed debt, saving them in their existing form. But it meant that many homeowners would slowly bleed out, and there would be millions of foreclosures and slow growth as normal people gradually repaired their balance sheets.

That was the underlying deal - losses got allocated to ordinary people. And the government embarked on a new industrial policy to replace some of the economic activity lost by housing, through the Fed inflating the stock market. Much of this activity was speculative, whether web 2.0, fracking, the gig economy, peak TV, or crypto. It was basically stuff that flourished on zero interest rates, with a lot of slack that depressed wages.

Are we set up for 2008 again? I don’t think so. First, we’re not going to be surprised by a bubble popping. There are discussion of it every day by business reporters. More importantly, there just doesn’t seem to be that much leverage in the system. Today Wall Street is worried about something called “private credit,” which is basically unregulated shadow bank lending to companies, and that’s a few trillion dollars. A lot of that is going to the AI data center buildout. So there is some reason for concern.

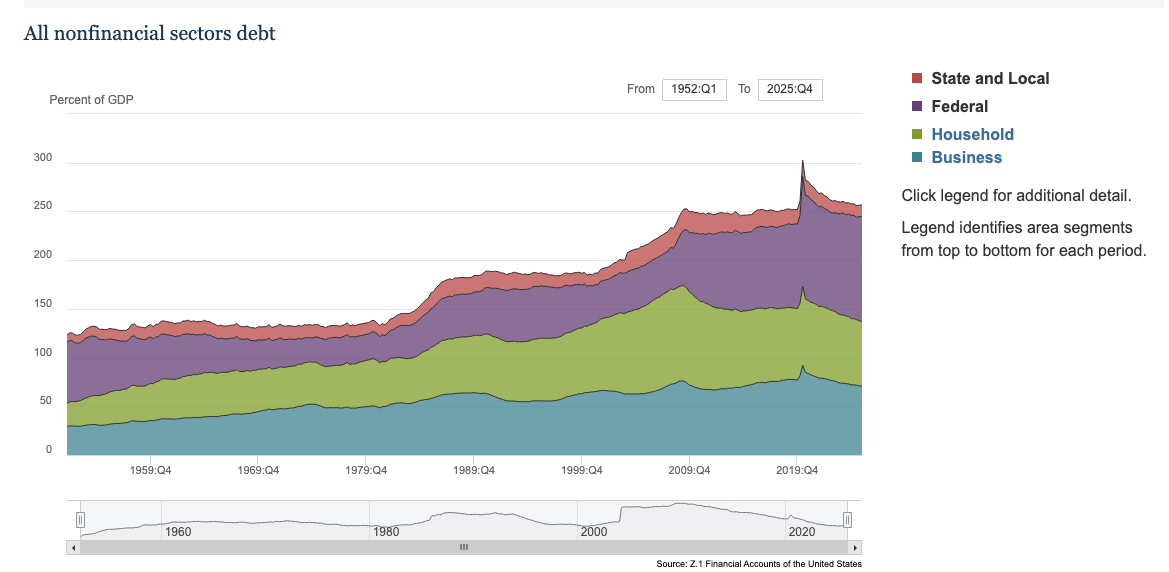

That said, it’s not like 2007, when there was four times as much private debt than government debt. Today it’s much more balanced, with a little more private than government debt - $32 trillion of Federal debt, and $20 trillion of household debt, and $22 trillion of commercial debt. Treasury bonds are “safe” insofar as government can print money to pay them. So it’s hard to see a financial crisis brewing based on gambling with other people’s money in the same way it happened back then.

Here’s a Federal Reserve’s chart of the broad debt owed by Americans, and you can see that most of it today is safe Federal debt, while during the 2008 crisis it was mostly riskier household debt.

Is It a Rerun of the Dot Com Crash?

A different analogy is the 2000-2002 crash of the dot com bubble that threw us into a recession. That one was the popping of a giant telecom build-out, which is similar to the AI data center build-out because we were investing in infrastructure.

The backstory was a roaring stock market that had gone steadily upwards since the early 1990s. And that was policy driven. The Fed implemented something called the “Greenspan put’” after the 1987 crash, in which Fed Chair Alan Greenspan rescued the stock market. Market participants believed they had an implicit guarantee from the Fed to bail them out of significant losses. There was financial deregulation, and new laws like the 1995 Private Securities Litigation Reform Act, made it easier for corporate CEOs to issue misleading statements.

Unlike 2008, this bubble was not a surprise. Greenspan himself noted ‘irrational exuberance’ in 1996, four years before it popped. The actual mechanism for the collapse was over-investment. A company called WorldCom was laying large amounts of fiber-optic networks, and other telecoms began massively doing so as well to keep up. In 2002, WorldCom was busted for one of the biggest accounting scandals of all time. The company had claimed that ordinary expenses were capital investment in broadband networks. The boom in fiber, in other words, was a result of fraud.

That said, there was much more than just fraud in one company. A whole sector, the internet, saw inflows of speculative capital, much of which ended up building useful projects, but much of which was wasted. From 2000-2002 the tech-heavy NASDAQ dropped by 77%, and more high-profile stocks like Amazon fell by 90%. There were other elements as well. The 9/11 attacks affected the economy, and a bunch of investment in fixing the Y2K problem dried up. But there wasn’t a lot of debt in the economy, so after a dip in business investment, centered around tech, telecom, and manufacturing, the recession ended.

The end of the dot com boom, like the 2008 crisis, saw the government replace the economic activity lost by investment in fiber and IT. The Fed cut rates, relaxed lending standards, thus engineering the housing boom that would eventually crush the economy a few years later.

The dot com analogy is a better one. The AI data center build-out is fostering significant economic growth, JP Morgan says it contributed 1.1% in the first half of 2025, “outpacing the U.S. consumer as an engine of expansion,” analyst Paul Kedrosky says it’s somewhere between 1.6% and 2.1%. These are very large numbers. If they collapse, we could see an investment-led recession, similar to 2000-2002. But it’s not a particularly leveraged economy, and no one will be surprised if the bubble pops.

The AI-Driven Stock Market Contagion

All that said, I think that an AI bubble popping could be worse than the dot com bubble, for a few reasons. The first is that we are a much more corrupt society, and so there will be less trust when a collapse happens and contagion is widespread. The second is the U.S. economy is less diversified today. We had a much stronger industrial base in 2000. Our financial markets are dependent on a few companies betting on AI data center spending. The counter-argument is that we are better at bailouts, so the Fed could stop contagion more easily. That’s possible too.

What are the specifics of what could happen in a collapse? Let’s go into different forms of contagion.

(1) Contagion to Workers Building Data Centers

While there is some employment around AI and data center buildouts, there isn’t that much of it. It is, as the Wall Street Journal noted, a “job-creation bust.” So I’m not that worried about the direct labor impacts of a decline in this activity, these aren’t railroads with huge workforces using pickaxes and driving trains. There are welders and HVAC specialists, but most of the chips are imported. I could be wrong, there are likely unexpected hidden links between our industrial firms and the data center buildout. But the direct pain will be felt in Taiwan and South Korea, who make most of the high-end stuff the data centers are buying.

(2) Consumer Contagion

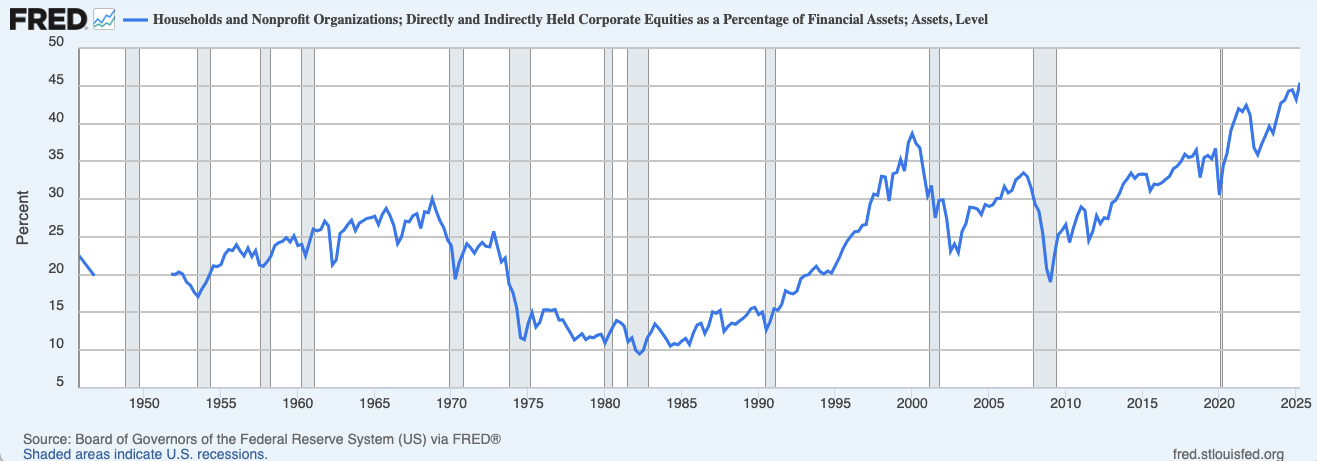

I do think there is going to be significant impact on consumers. Americans have never been more dependent on the value of the stock market. Forty five percent of what we own is in stocks, which is significantly higher than it was in 2000. And AI stocks are something like 75% of returns to the stock market since 2022, and 80% of earnings growth. So we’re talking about significant hits to 401(k)’s and retirement accounts.

Most stocks are owned by the wealthy, who are supporting consumer spending. But how much does wealth translate into spending?

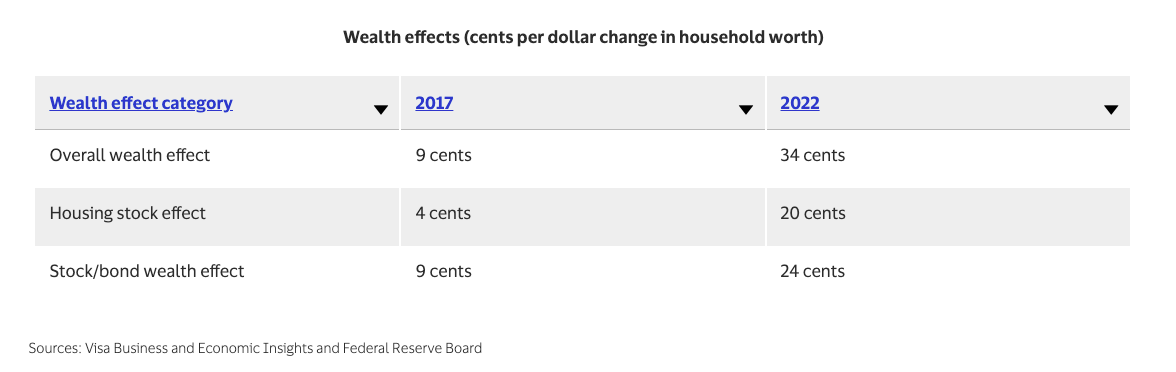

To understand that, we have to look at something called the “wealth effect,” which is how much an increase or decrease in your asset values transforms into additional or less consumer outlays. As I noted in September, the wealth effect didn’t used to be significant. “Prior to the 1980s, people might sock some money away for retirement or a rainy day, and the stock market didn’t matter much to their immediate spending. What did matter was whether you get a raise or a bonus. So the wealth effect was low, an increase of stock market wealth didn’t affect consumer spending.

If, however, asset appreciation becomes something that people get used to as a form of compensation, then the wealth effect should grow. And that’s what we’ve seen. During the Covid stock market spike in 2022, the wealth effect increased dramatically. Visa put out some numbers on the phenomenon.”

According to our estimates, the wealth effect between 2002 and 2017 was 9 percent. Said another way, for every $1 increase in household wealth, consumer spending increased by 9 cents. Over the last few years, however, something changed dramatically. Using data through the third quarter of 2022, we find that the wealth effect has increased to 34 cents, almost quadruple the pre-pandemic average.

These are very big numbers. We can expect a significant decline in consumer spending if the stock market drops substantially.

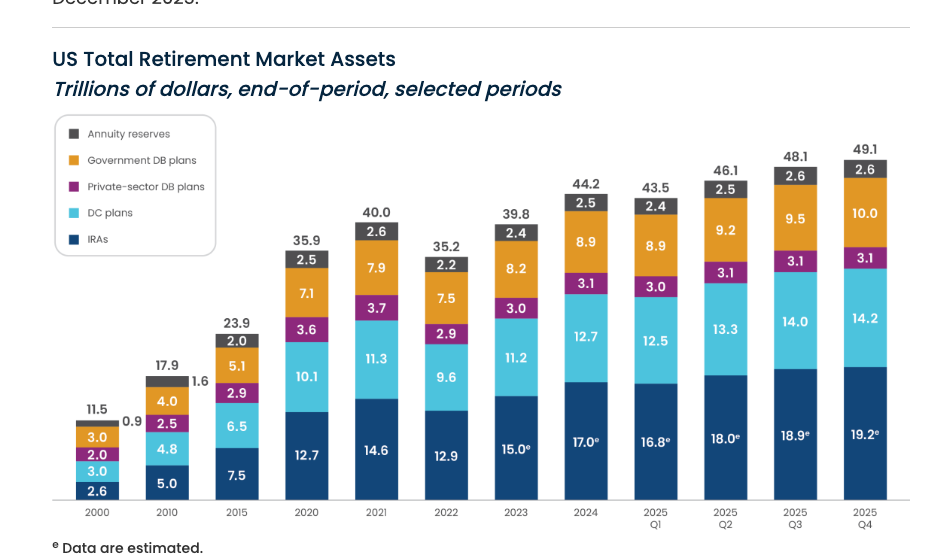

(3) Retiree Contagion

There’s $50 trillion in retirement assets, a majority of it in investment portfolios for individuals, but some of it in pensions. Retirees will have less spending power, and some will see their pensions cut or eliminated.

(4) Private Equity Contagion

The stock market isn’t just a higher percentage of financial assets, it’s a much more important benchmark for a whole set of private markets. There is, for instance, private equity. These are financial institutions that get money from rich people, insurance companies, university endowments, and other pools of capital, and invest it in portfolio firms, housing, or other assets.

McKinsey says that PE controls about $23 trillion in assets under management, which is 20 times its size in 2000. PE firms value the companies they own by referencing them to public companies, so a collapse in the stock market will cause significant problems for that sector. Not all of private equity is in domestic portfolio companies, but it’ll get hit, and hit hard.

If private equity freezes up, on the portfolio side, you can expect them to put their companies into bankruptcy, since they tend to run their firms with too much debt. You can also expect layoffs and attempts to squeeze blood from a stone. On the investor side, private equity funds will likely demand that their institutional partners - again universities, rich people, and insurance companies - hand over capital for investment. (Being on the hook for capital is one of the perils of investing in private equity.) So that’s going to put pressure on these institutions to sell what they can to meet private equity calls.

(5) Academic Contagion

Many important nonprofit institutions, from universities to foundations, are invested in private equity and private credit, as well as equity markets. The Federal Reserve Flow of Funds says that nonprofits have roughly $14 trillion in assets on their balance sheet.

These institutions often pull a set percentage of their portfolios every year for annual outlays. If these portfolios are lower in value, well, that’s less spending. So we will see academic centers and nonprofits take a hit. Cities dependent on universities will see layoffs.

(6) State and City Contagion

This year, California is seeing revenue running $16.5 billion above projections, largely because of capital gains due to the stock market run-up. They have reserves, but not enough to weather a crash. New York City too is now heavily dependent on AI spending, and not just Wall Street.

Many states and cities by law have to balance their budgets, and lower capital gains means they will have to cut spending. So we can expect to see declines in local and state government employment.

(7) Global Contagion

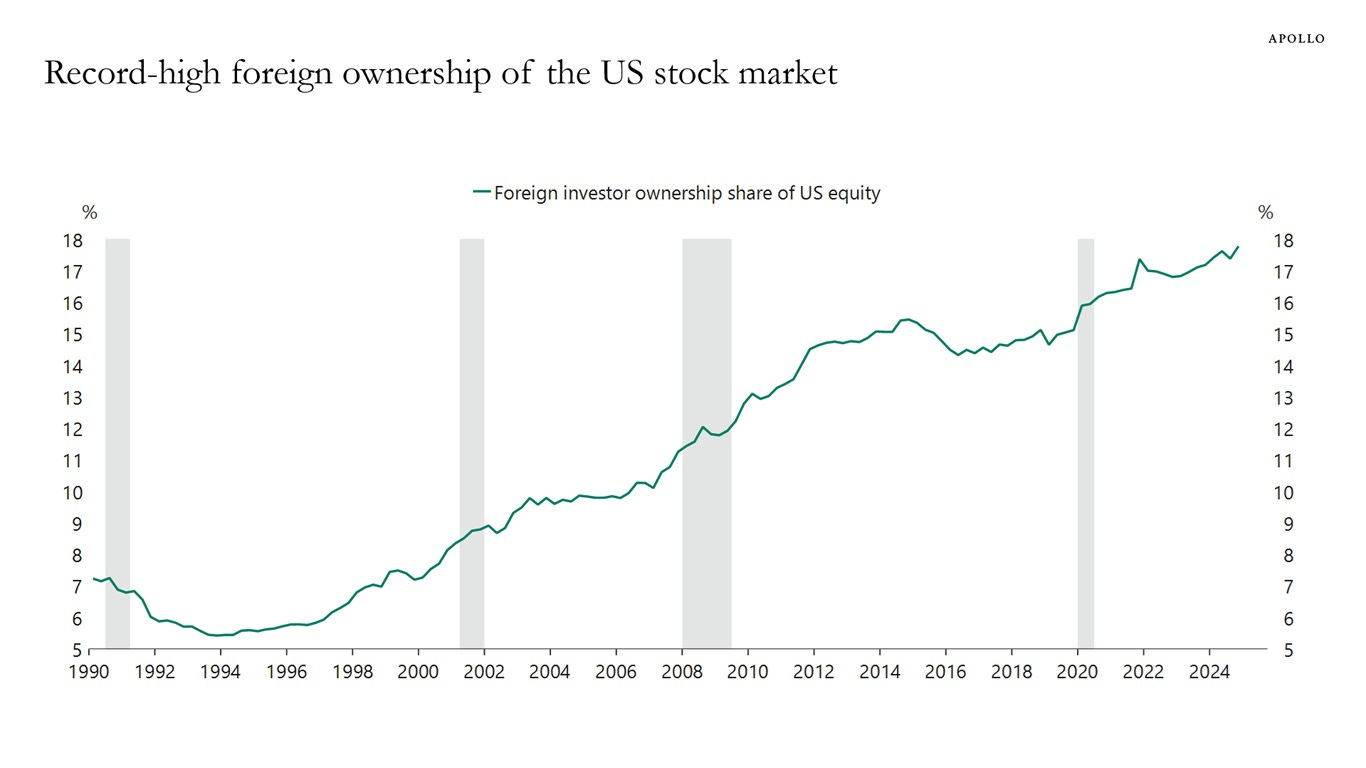

There’s also the foreign policy aspect of the situation. South Korea, Japan, and Taiwan have insane export surpluses with the U.S., largely based on them sending us AI-related information technology and chips to go into our data centers. Their economies will get hit hard, and they will likely have to liquidate portfolios of dollar-denominated assets, like U.S. government debt.

Beyond the AI-related imports, the U.S. brings in about a trillion dollars worth of stuff more than we export. Why do people keep selling us stuff without selling anything back to them? Well, they want to buy dollar-denominated assets, and to enable that, we have to run a big trade deficit. Today, foreigners own 18% of the U.S. stock market, and everyone invests in American monopolies as a part of their portfolio.

If these investments collapse in value, well, the global financial and foreign policy architecture will be put under strain. In 2008, Hank Paulson went to China to convince them not to sell Fannie and Freddie bonds, which would have caused more turmoil on Wall Street. What happens if Nvidia, Google, Amazon, and Microsoft lose half of their value? They’ll still be massive, but you’ll have a bunch of Middle Eastern princes, foreign oligarchs, Japanese and Taiwanese investors, and European pension funds losing a lot of money, with all that implies.

(8) Bezzle Contagion

In environments characterized by corruption, fraud tends to flourish. And in a down market, that can be very scary. Here are three examples to help us understand what that might feel like

In 2015, hip hop legend Russell Simmons presided over a financial scandal when his prepaid debit card empire - RushCards, had a “glitch.” Roughly 100,000 customers, many of whom were unbanked but trusted Simmons, couldn’t access their money.

In 2024, Synapse, a fintech company, collapsed, stranding another 100,000 customers and $265 million held across a bunch of platforms. The banks that worked with Synapse couldn’t get access to accurate records, for months.

In 2025, private equity financed auto parts distributor First Brands collapsed in an orgy of fraud, a “cockroach” in the industry.

The day before these frauds were revealed, the victims would not know they are going to be out of luck. If you had a RushCard with $50 on it, you’d think, “I have $50.” But the fraudster would know he is committing fraud. The next day, you’d realize you have nothing. Economist John Kenneth Galbraith coined a term to describe this quasi-value, known as the “bezzle” (after the term embezzlement). The bezzle is the amount that a victim thinks he has until the fraud is revealed.

In a crisis, all sorts of frauds get exposed, because people need access to their money. It’s not a coincidence that Bernie Madoff was undone in the 2008 crisis; he was running a standard Ponzi scheme unrelated to the crisis, but the liquidity needs of his customers killed his scam.

Given the nature of how DOGE and the Trump administration has hollowed out the regulatory state, I suspect that we will see significant revelations of fraud. The fintech Sofi, which is quite popular, is being scrutinized by short-sellers. And we might be in a situation where important institutions like the FDIC, which insures bank accounts, is simply unstaffed or incompetent or otherwise unwilling to help even if it’s legally obligated to do so.

So yeah, we could see bank runs.

(9) Strains on Real Estate and Utilities

As the Center for Public Enterprise pointed out, data centers are not just investment, they are also a real estate play. So real estate assets might take a hit. In addition, utilities have planned to build more power generation and delivery infrastructure, if the data centers don’t get constructed as planned, we could see financial strain on that sector. That mal-investment needs to be paid for, so either ratepayers will pay for it, or utility shareholders will take a hit.

The Politics of an AI Crash

Crashes are really awful experiences, but they also reveal the hidden patronage networks that tie together our economy. If the AI bubble cracks, there will be political pressure from all sorts of corners to encourage the government to bail out data centers and double down on our finance-led model, effectively allocating the losses to someone else.

This pressure will come from the unions whose members build data centers, pension fund managers panicking about their losses, universities and academics whose budgets have been crushed, private equity firms, life insurance companies who can’t pay out policyholders, retirees who have lost their 401(k)s, the superrich, foreign diplomats trying to rescue what they can from their dependence on U.S. financial markets, national security officials worried about the stability of their AI vendors, and industrial firms who have become important parts of the data center buildout.

It may come from weird unexpected places. Imagine seeing NYC Mayor Zohran Mamdani and OpenAI’s Sam Altman both testifying for a new special purpose Fed facility to rescue municipal budgets tied to data centers. That could be a real possibility, if we don’t prepare.

Preparing for a Crisis

I’ve seen a number of financial crises in my time in politics, big ones like 2008 and Covid, and little ones, like the Silicon Valley Bank bailout. There is one important dynamic, a pervasive belief the losers will not be made whole, and so it’s absolutely critical not to be one of the losers even if that means maintaining an unfair and unbalanced system.

For example, we know most Americans do not have enough saved in their 401(k)s to have any decent form of retirement, and it would be much better if we simply substituted more Social Security payments or other guaranteed pension-like payments for individual speculation in the stock market. However, few people who have a retirement account believe that is likely, so they will desperately try to hold onto the modest amount they have. In a crash, they will panic, and try to restore their portfolio through political action.

This dynamic is true across the board. Corporate CEOs, mayors, university presidents, bankers, union leaders, and so forth, they all finance their institutions with lots of assets and lots of debt, instead of a more stable financial arrangement based on being able to pay out of their own institutional income for what their institution needs. In a crisis, theoretically it’s possible to wipe out asset values and debts and transition to paying through revenues, but that requires collective action and a willingness to share burdens. Few of them believe that is possible or preferable.

Our institutions are also set up to foster an oligarch-friendly bailout. Liberals mostly don’t pay attention to the Treasury Department and the alphabet soup of bailout programs set up by the Federal Reserve. Usually Fed programs are of two kinds. There are the real ones run for the benefit of Wall Street, and there are the fake ones set up to pretend that cities and small businesses should have financing. The fake ones are quietly shut down after no one takes advantage of their onerous terms. The Supreme Court recognized our bailout-friendly order by carving out a special Constitutional area for the ‘independence’ of the Federal Reserve.

I don’t want to overstate this situation. The Covid bailouts were much more fair than the 2008-2010 bailouts. Neither were fair, but the Covid-era Paycheck Protection Program kept millions of small business in operation, and individuals did get checks. By contrast, the response to the Great Financial Crisis was to help the rich and screw everyone else.

So the situation is getting better, as the public pays attention. In a crash, we could easily do what we did in the 1930s, and create a new government bank, the Reconstruction Finance Corporation. Since most private equity would be insolvent, we could wipe that whole financing model out, and make social decisions to restore a different kind of industrial policy. We could seek to build out health centers, a diversified industrial base, public investment in improving the welfare of families, better food systems, and a reorganization of supply chains to make things cheaper for everyday Americans.

Imagine a recruiting and financing plan to get tens of thousands of young people to start farms, and to restart food processors that used to marble the nation. And a mechanism to rebuild light manufacturing in electronics, along with changes to patents and trade to spread out innovation. Or a breakup of big tech ad monopolies, and financing for the formation of thousands of new newspapers. Or deploying better energy systems and electric systems of transportation. Or rebuilding New York City so it is a port-based hub of commerce and manufacturing again, instead of dependent on real estate and finance.

With the right political framework, we could just say ‘hey unions, here’s a bunch of Federal money to make up for most of your pension stock market losses.’ But that requires unions to believe that such a deal is possible, otherwise they will simply push for a bailout of AI firms in the hopes they will get scraps.

These are remarkable possibilities, if we can convince people there is hope on the other side of the losses. That’s what happened in the New Deal, but of course, it took four years from 1929-1933 of fights over how to allocate losses and a national calamity before newly elected leaders could sweep away the old order. And that’s a huge risk - in Germany the political turmoil of that calamity turned out, well, differently.

Predicting the end of bubbles is impossible, so this one could run on for years. But in my view, this AI bubble *should *pop. It’s a bad policy choice to focus most of our economic investment in data centers and copyright theft. This strategy is now so important to growth that President Trump is even supporting a moratorium on state regulation of AI, which is very bad idea.

That said, the end of financial bubbles is often dangerous and unpredictable. And I don’t have a lot of confidence the people who run our central banking order will recognize what to do. On the other hand, at least this time Larry Summers won’t be the architect of whatever we end up choosing.

In the comments, give me your thoughts. I’m particularly interested in where you see other areas of possible contagion.

Thanks for reading! Your tips make this newsletter what it is, so please send tips on weird monopolies, stories I’ve missed, or other thoughts. And if you liked this issue of BIG, you can sign up here for more issues, a newsletter on how to restore fair commerce, innovation, and democracy. Consider becoming a paying subscriber to support this work, or if you are a paying subscriber, giving a gift subscription to a friend, colleague, or family member. If you really liked it, read my book, Goliath: The 100-Year War Between Monopoly Power and Democracy.

cheers,

Matt Stoller

这条对你有帮助吗?